In terms of applying the tax on a per room basis, this will be difficult to implement in different accommodation models. How would it apply to youth hostels with multiple beds per room / single occupancy in a two-room apartment / rogue operators who over- occupy properties?

A seasonal charge would exacerbate the administrative burden of a tourism tax.

Is the income worth the investment to implement the scheme properly and efficiently?

A tourism tax is not intended to fund core services. A tourism tax should support the key priorities set out by The Scottish Tourism Alliance’s Tourism Scotland Strategy 2020.

Any investment should be able to be measured, and the impact clearly identified.

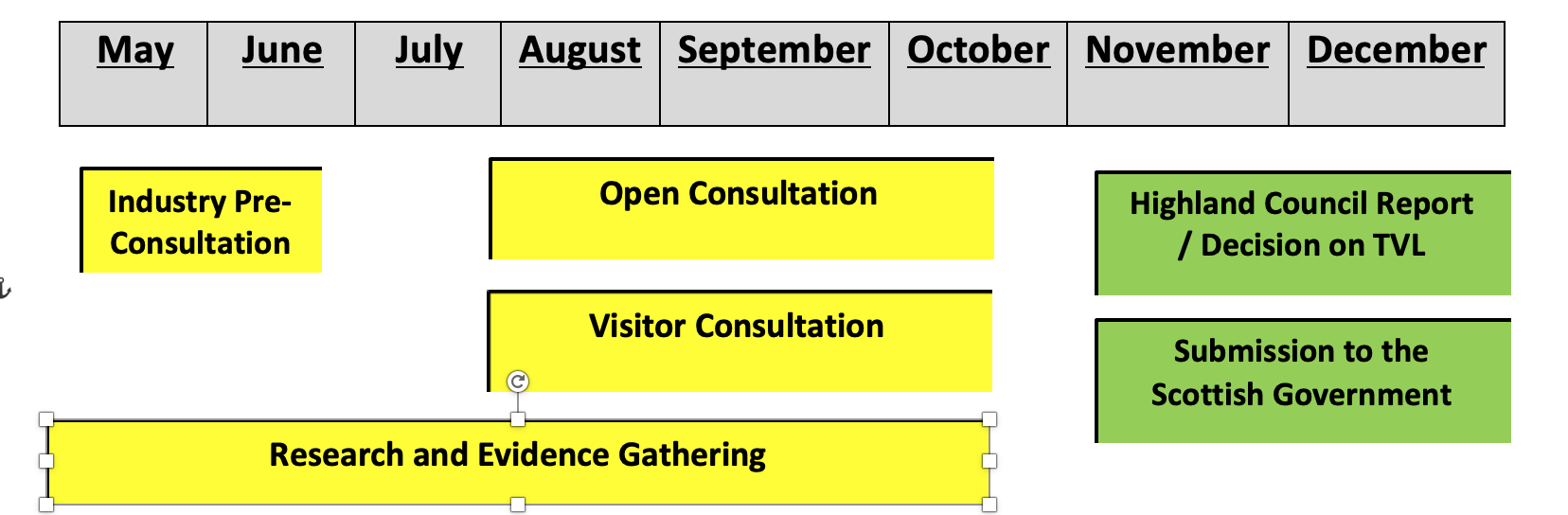

Out-with the administration of a tourist tax, consideration should still be given to:

There has been no economic impact assessment of how a tourist tax would impact on visitor spend / businesses administrative costs / local authorities to implement.

The potential reputational damage it may have to Scotland and visitors’ perception of our ‘welcome’.

It should not be a solely a ‘bed tax’, which will penalise overnight visitors, while excluding letting day visitors. Several sectors should contribute to any levy.

Alternative approaches to a levy should be considered reflecting a diverse range of requirements across the 32 local authorities: car parking charges, number plate recognition, events and festival tickets etc

73% of ASSC members are opposed to a tourist tax.

In rural areas with plenty of capacity, operators are not able to charge city rates or let by the night.

If rural businesses are forced into increasing their prices further that it could seriously damage these small businesses.

There is a finer economic balance in rural parts, especially in remoter areas.

Proponents of a tourism tax frequently assert that they successfully operate in a number of European cities, while simultaneously failing to acknowledge the high rate of VAT applied to our sector.

In uncertain times, with Brexit on the horizon and many sectors anticipating a downturn, bringing in an additional tax at this stage would potentially be negligent.